PCI DSS Compliance: Unlocking Bigger UK Contracts

- Gary Sinnott

- Feb 11

- 7 min read

Protecting payment card data is no longer just an IT concern for UK e-commerce businesses aiming to grow and secure larger contracts. The shift to PCI DSS 4.0.1 means data protection now demands ongoing scrutiny and adaptability, not simple box-ticking. For IT directors at British SMEs, getting compliance right helps build lasting customer trust and keeps operations running smoothly. This guide breaks down what matters most in maintaining robust cardholder security and staying competitive in a fast-changing regulatory environment.

Table of Contents

Key Takeaways

Point | Details |

Ongoing Compliance | PCI DSS compliance is a continuous process, requiring businesses to adapt their security measures regularly to address emerging threats. |

Merchant Levels | Compliance requirements vary by merchant level, determined by annual transaction volumes, impacting assessment methods. |

Reputational Risks | Non-compliance can result in severe reputational damage, making robust cybersecurity a vital business differentiator. |

Financial Consequences | Businesses face significant financial penalties for non-compliance, highlighting the importance of proactive risk management strategies. |

PCI DSS compliance explained in 2026

PCI DSS (Payment Card Industry Data Security Standard) remains a critical framework for protecting payment information in the United Kingdom. At its core, the standard provides comprehensive guidelines for securing card transaction processes and preventing potential data breaches. By 2026, data protection has become increasingly sophisticated, requiring businesses to implement robust cybersecurity measures beyond traditional compliance checklists.

The standard encompasses several key areas of protection for businesses processing card payments:

Maintaining secure network infrastructure

Protecting cardholder data through encryption

Implementing strong access control mechanisms

Regularly monitoring and testing security systems

Developing comprehensive information security policies

For UK small and medium enterprises (SMEs), cardholder data security represents more than a regulatory requirement. It’s a strategic business imperative that directly impacts customer trust and organisational reputation. The evolving landscape of cyber threats means businesses must continuously adapt their security approaches to stay ahead of potential vulnerabilities.

Understanding the nuanced requirements of PCI DSS in 2026 involves recognising that compliance is an ongoing process, not a one-time achievement. Organisations must demonstrate continuous improvement in their security frameworks, with regular assessments and updates to their protection strategies. This dynamic approach ensures that businesses remain resilient against emerging cyber risks while maintaining the integrity of payment transactions.

Pro tip: Conduct quarterly internal audits of your payment processing systems to proactively identify and address potential security gaps before they become critical vulnerabilities.

Levels, self-assessment types and validation options

PCI DSS compliance is not a one-size-fits-all approach, with different validation requirements based on the volume and complexity of an organisation’s card transactions. The standard categorises merchants into four distinct levels, each with specific assessment and reporting obligations. These levels help tailor the compliance process to the scale and risk profile of different businesses.

The merchant levels are determined by annual transaction volumes:

Level 1: Over 6 million card transactions per year

Level 2: 1-6 million card transactions annually

Level 3: 20,000-1 million e-commerce transactions

Level 4: Less than 20,000 e-commerce transactions or up to 1 million total transactions

Validation requirements for compliance vary significantly across these levels. Smaller merchants typically complete self-assessment questionnaires (SAQs), while larger organisations require comprehensive on-site assessments by a Qualified Security Assessor (QSA). These assessments evaluate the organisation’s security controls, network infrastructure, and data protection mechanisms.

Self-assessment questionnaires provide a structured approach for merchants to evaluate their compliance status. There are multiple SAQ types, including SAQ A for e-commerce merchants, SAQ B for point-of-sale environments, and more complex versions for organisations with more intricate payment processing systems. The key is selecting the most appropriate questionnaire that reflects the specific payment acceptance method and technology environment.

Here’s a summary of PCI DSS merchant levels and their typical validation requirements:

Merchant Level | Typical Annual Transactions | Assessment Method | Validation Documentation |

Level 1 | Over 6 million | On-site QSA audit | Formal Report on Compliance |

Level 2 | 1 to 6 million | SAQ or QSA audit | SAQ or Report on Compliance |

Level 3 | 20,000 to 1 million (e-commerce) | SAQ | SAQ and quarterly scan |

Level 4 | Fewer than 20,000 (e-commerce) or up to 1 million (total) | SAQ | SAQ and scan if required |

Pro tip: Consult with a PCI DSS specialist to determine the most appropriate self-assessment questionnaire for your specific business model and transaction processing environment.

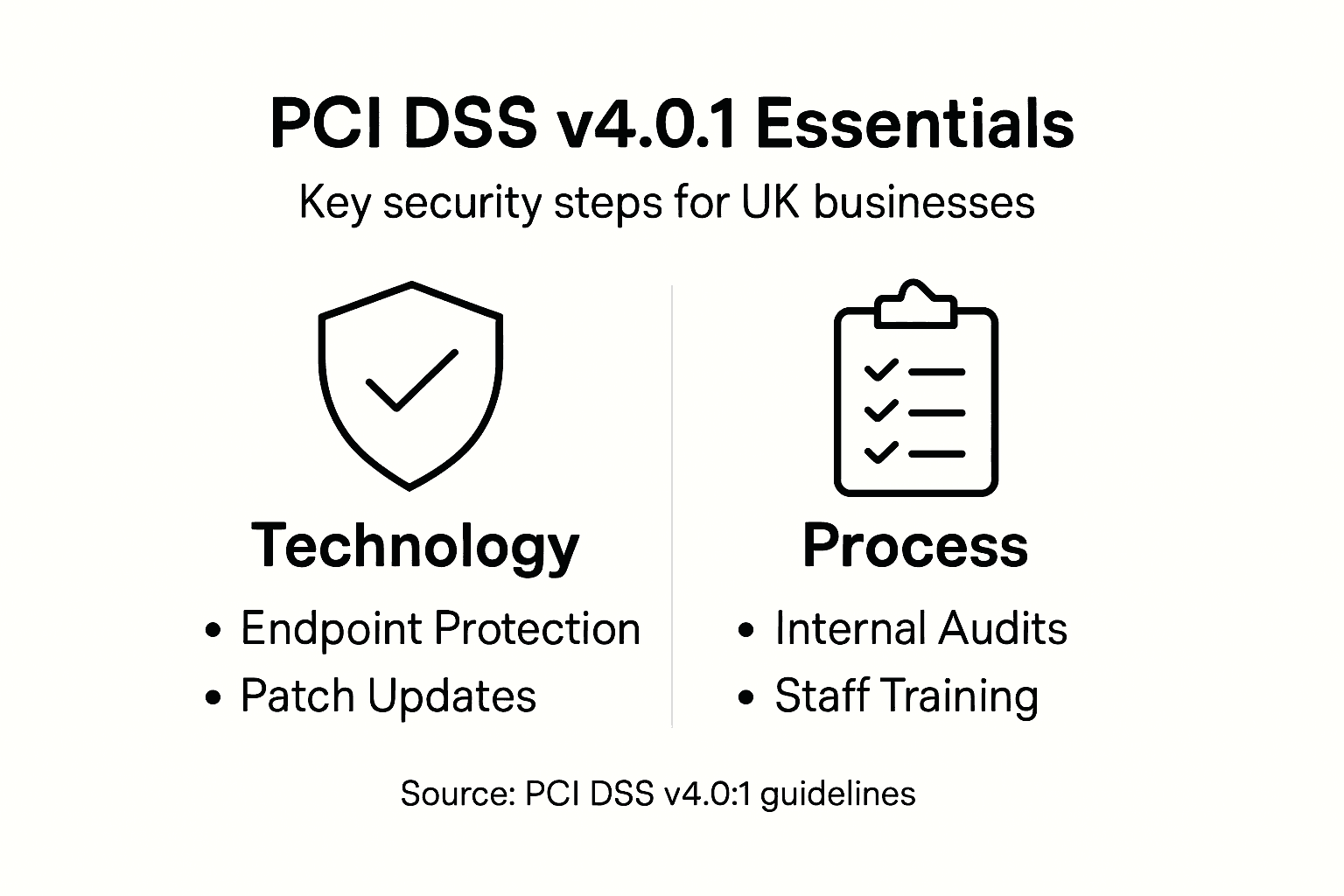

Key requirements of PCI DSS v4.0.1

PCI DSS version 4.0.1 represents a significant evolution in cybersecurity standards for payment card processing, introducing more flexible yet rigorous requirements for organisations handling sensitive financial data. The updated framework emphasises a proactive and dynamic approach to security, moving beyond static compliance checklists towards continuous risk management and adaptive protection strategies.

The core requirements of PCI DSS v4.0.1 focus on several critical security domains:

Robust access control mechanisms

Advanced encryption protocols

Comprehensive vulnerability management

Continuous network monitoring

Detailed logging and tracking of security events

Regular security awareness training

Cybersecurity in payment systems now demands more than traditional defensive measures. Organisations must implement multi-factor authentication, develop sophisticated risk assessment procedures, and demonstrate ongoing security improvements. The standard requires merchants to establish a security-first culture that goes beyond mere technical controls, embedding protection into every operational process.

Key technological requirements include implementing advanced endpoint protection, maintaining up-to-date patch management processes, and conducting regular penetration testing. Organisations must also develop comprehensive incident response plans that outline precise steps for detecting, containing, and mitigating potential security breaches. This holistic approach ensures that businesses can effectively protect cardholder data while maintaining operational resilience.

Pro tip: Develop a comprehensive security roadmap that aligns PCI DSS v4.0.1 requirements with your organisation’s unique technological ecosystem and risk profile.

Legal obligations and reputational risks for SMEs

Navigating the complex landscape of legal obligations surrounding payment card data protection represents a critical challenge for UK small and medium enterprises. Regulatory compliance is no longer optional but a fundamental requirement for businesses processing financial transactions, with potential consequences extending far beyond mere financial penalties.

The key legal risks for SMEs include:

Substantial financial penalties up to £17.5 million or 4% of annual turnover

Potential mandatory public reporting of data breaches

Loss of merchant payment processing capabilities

Permanent damage to business reputation and customer trust

Potential criminal liability for senior management

Data protection requirements have become increasingly stringent, particularly under the UK Data Use and Access Act 2025. SMEs must recognise that non-compliance is not merely a regulatory checkbox but a fundamental risk management strategy that directly impacts business sustainability and market credibility.

Reputational damage can be even more devastating than direct financial penalties. A single data breach can erode customer confidence, leading to contract terminations, negative media coverage, and long-term brand erosion. Prospective clients and partners increasingly view robust cybersecurity as a key differentiator when selecting business partners, making PCI DSS compliance a critical competitive advantage for forward-thinking SMEs.

Pro tip: Develop a comprehensive incident response plan that demonstrates your commitment to data protection, enabling swift and transparent communication in the event of potential security challenges.

Costs, penalties and common pitfalls to avoid

Navigating the financial landscape of PCI DSS compliance requires a strategic understanding of potential costs and penalties that can significantly impact UK small and medium enterprises. Financial risk extends beyond immediate monetary penalties, encompassing long-term business sustainability and operational continuity.

The most critical financial and operational risks include:

Potential fines up to £17.5 million or 4% of annual global turnover

Immediate suspension of merchant payment processing services

Mandatory breach notifications and potential legal proceedings

Substantial costs for forensic investigations and system remediation

Potential criminal liability for senior management

Compliance enforcement mechanisms demonstrate the rigorous approach regulatory bodies take towards data security breaches. Common pitfalls that SMEs frequently encounter include inadequate risk assessments, incomplete documentation, delayed incident response, and insufficient staff training.

The most prevalent compliance mistakes can be categorised into three primary areas: technological vulnerabilities, procedural gaps, and human error. Technological vulnerabilities often stem from outdated systems, unpatched software, and weak encryption protocols. Procedural gaps emerge from inconsistent security policies, lack of regular audits, and inadequate access control mechanisms. Human error remains the most unpredictable risk, with employees inadvertently compromising security through poor password management, falling for phishing attempts, or mishandling sensitive data.

Understanding the main areas of PCI DSS risk can help SMEs target improvements effectively:

Risk Area | Example Pitfall | Potential Impact |

Technological Weakness | Outdated software or systems | Heightened breach risk |

Procedural Deficiency | Missing regular audits | Non-compliance fines |

Human Error | Weak password practices | Accidental data exposure |

Pro tip: Implement a comprehensive security awareness programme that transforms compliance from a technical requirement into an organisation-wide cultural commitment.

Unlock Bigger UK Contracts with Trusted PCI DSS Compliance Support

Achieving PCI DSS compliance is a major step for UK SMEs striving to expand their business and win high-value contracts. The challenge lies not just in meeting the requirements but transforming compliance into a strategic business asset that highlights your organisation’s commitment to data security and digital resilience. From understanding complex frameworks to managing risks and continuous monitoring, this journey can feel overwhelming without the right expertise.

Let Freshcyber guide you beyond paperwork with our Compliance solutions designed specifically for ambitious SMEs.

Take control of your security roadmap with our vCISO-led Compliance Currency Engine that delivers executive-level leadership and multi-framework management all under a single subscription. Combine this with robust Vulnerability Management and proven Cyber Essentials certification support to turn security into your strongest sales asset. Visit Freshcyber today and start scaling with confidence and credibility.

Frequently Asked Questions

What is PCI DSS compliance and why is it important?

PCI DSS compliance refers to the Payment Card Industry Data Security Standard, which provides guidelines for securing payment information. It is crucial for protecting cardholder data and maintaining customer trust, especially for businesses processing card transactions.

How can PCI DSS compliance help unlock bigger contracts?

Achieving PCI DSS compliance demonstrates a commitment to data security and risk management, which can enhance business credibility. Many larger organisations only partner with compliant vendors, potentially leading to access to bigger contracts and opportunities.

What are the different levels of PCI DSS compliance?

PCI DSS compliance is categorised into four levels based on annual transaction volumes. Level 1 involves over 6 million transactions, while Level 4 includes fewer than 20,000 e-commerce transactions or up to 1 million total transactions.

What are the common pitfalls SMEs face in achieving PCI DSS compliance?

Common pitfalls include inadequate risk assessments, incomplete documentation, delayed incident responses, and insufficient staff training. Additionally, technical vulnerabilities and human errors, such as weak password practices, can lead to significant compliance challenges.

Recommended